In the bustling world of global commerce, Small and Medium-sized Enterprises (SMEs) stand tall as pivotal players. They're not just businesses; they're the lifeline of the economy, creating jobs and spurring innovation. Yet, when it comes to SME banking, they often find themselves in choppy waters.

As the World Bank’s database acknowledges, SMEs are less likely to be able to obtain bank loans than large firms. Instead, they rely on internal funds, or cash from friends and family, to launch and initially run their enterprises, leading to a variety of challenges when navigating banking territory. The quandaries become even more prominent when micro and informal enterprises join the big picture.

Enter FinTech, transforming the landscape with its digital prowess. This article explores how it reshapes the financial world with SME banking software, addressing the businesses’ unique needs and opening up a world of possibilities.

What is SME Banking?

SME banking is a set of financial services custom-fitted for the smaller scale and specific needs of Small and Medium-sized Enterprises (SMEs).

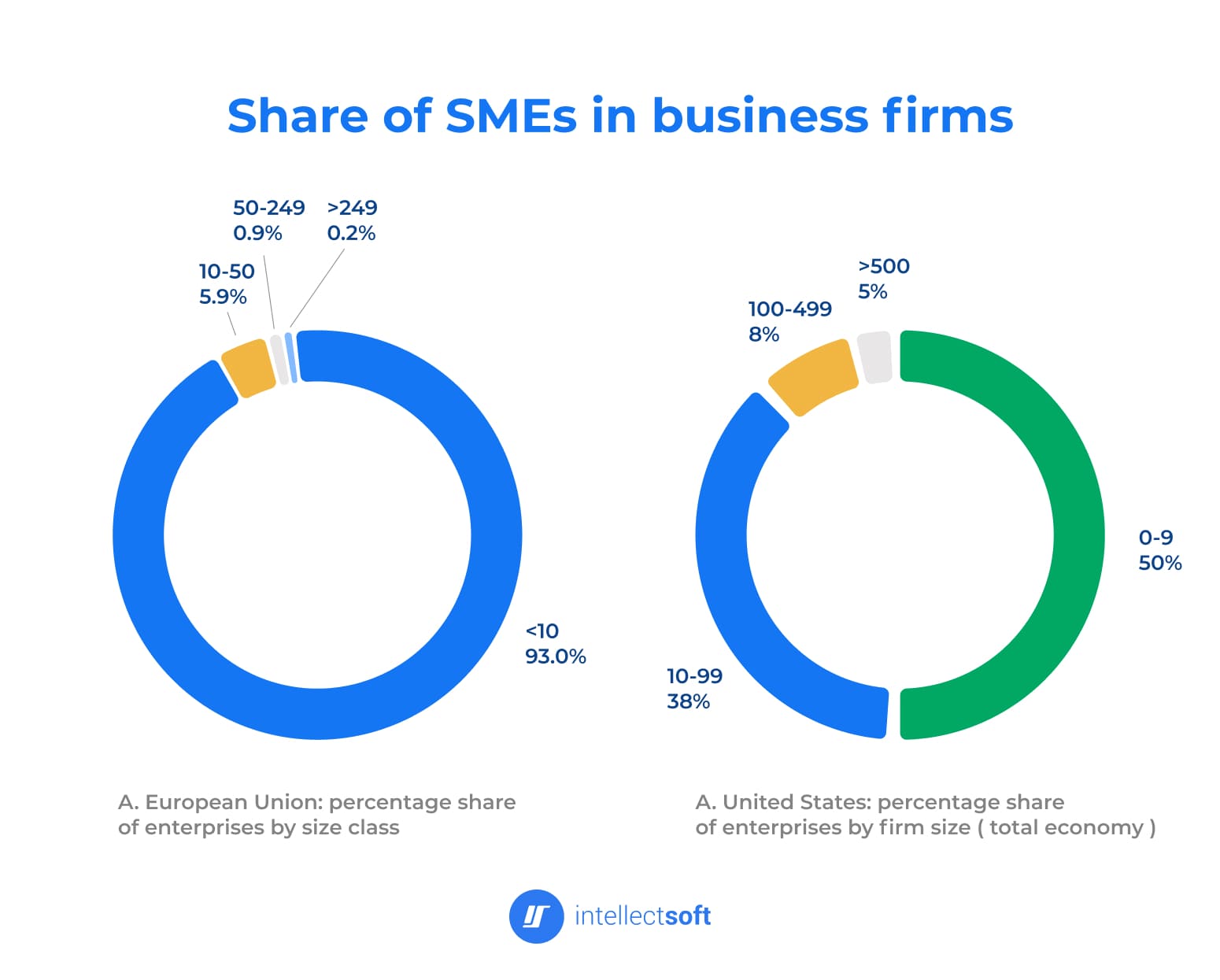

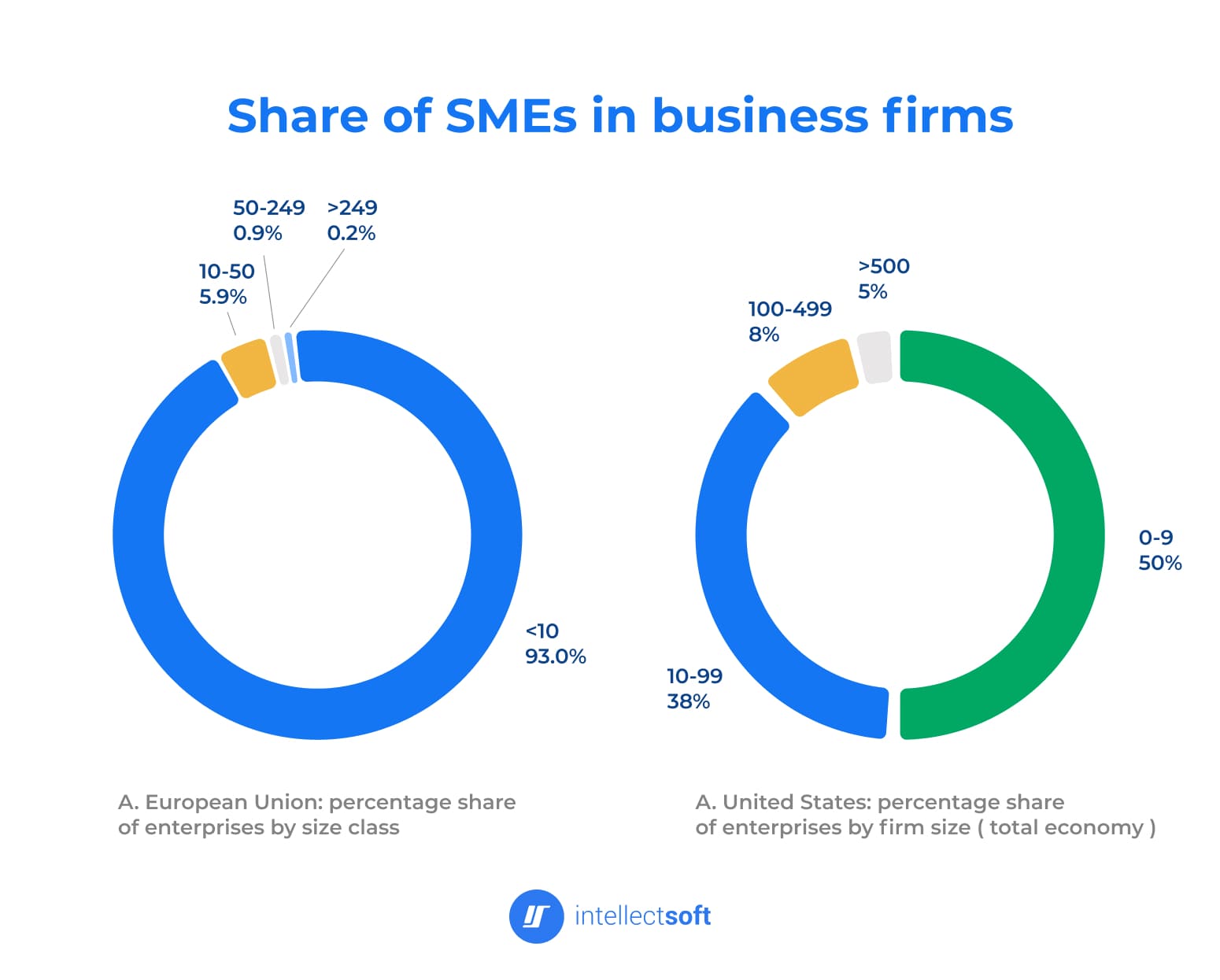

What makes it important? According to the OECD, SMEs account for over 95% of firms and 60%-70% of employment. They also generate a large share of new jobs in the OECD economies.

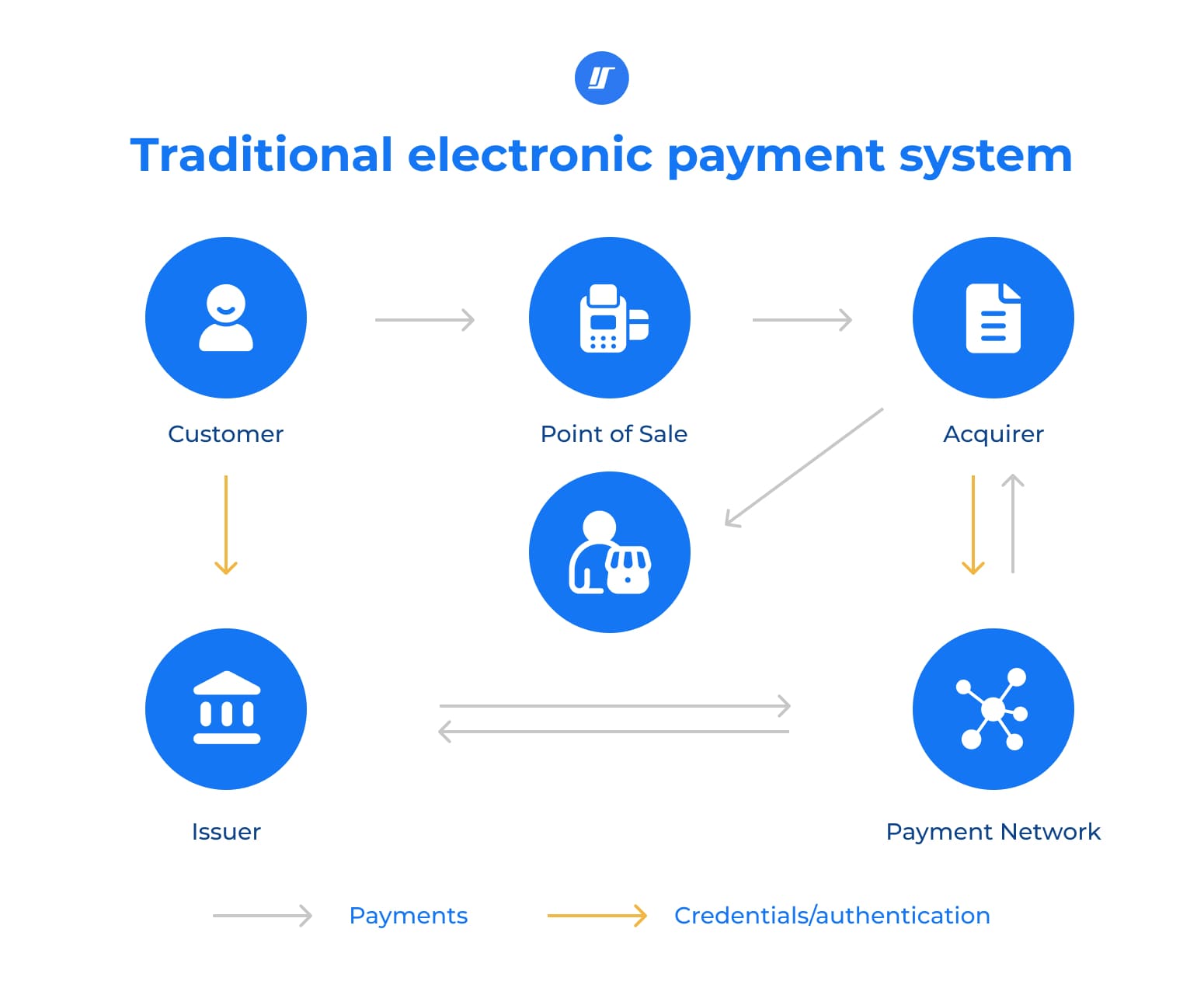

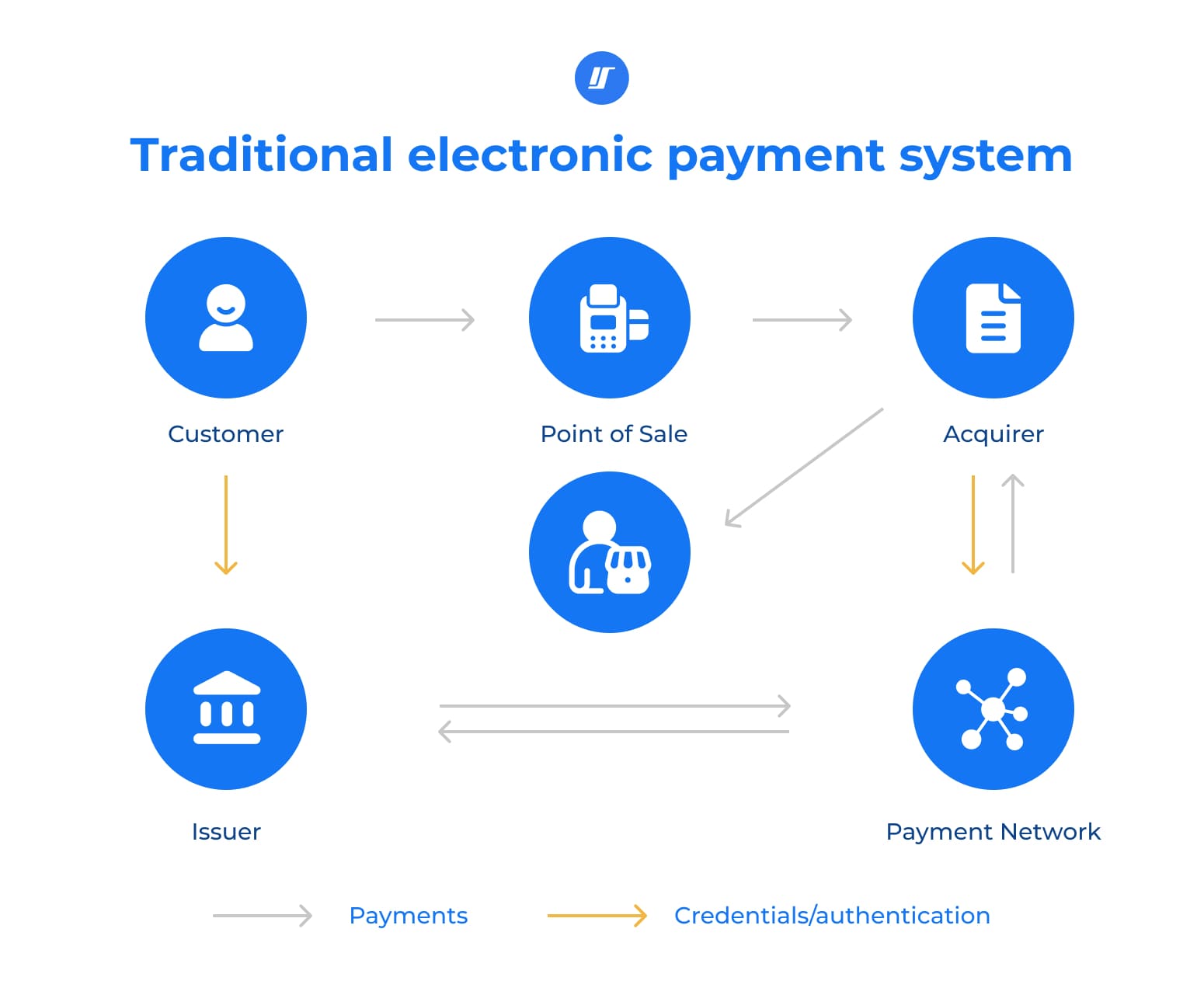

Traditional banking services like loans, credit lines, and deposit accounts have been gradually sculpted to fit SMEs' demands and industrious nature. However, the journey wasn't straightforward. In the not-so-distant past, SMEs faced a banking landscape that was, more often than not, below accommodating. Navigating the traditional banking terrain felt like trying to solve a Rubik's cube blindfolded.

SMEs grappled with high fees, rigid credit assessments, and optimized one-size-fits-all solutions that barely fit anyone in practice. Securing funding was akin to a Herculean task, while personalized financial advice was rare and often accessible only to the privileged minority.

The disconnect between what SMEs needed and what banks offered was glaring. It was this very gap, this misalignment of services, that set the stage for the FinTech revolution that promised to tear down these barriers and usher in a new era of customization.

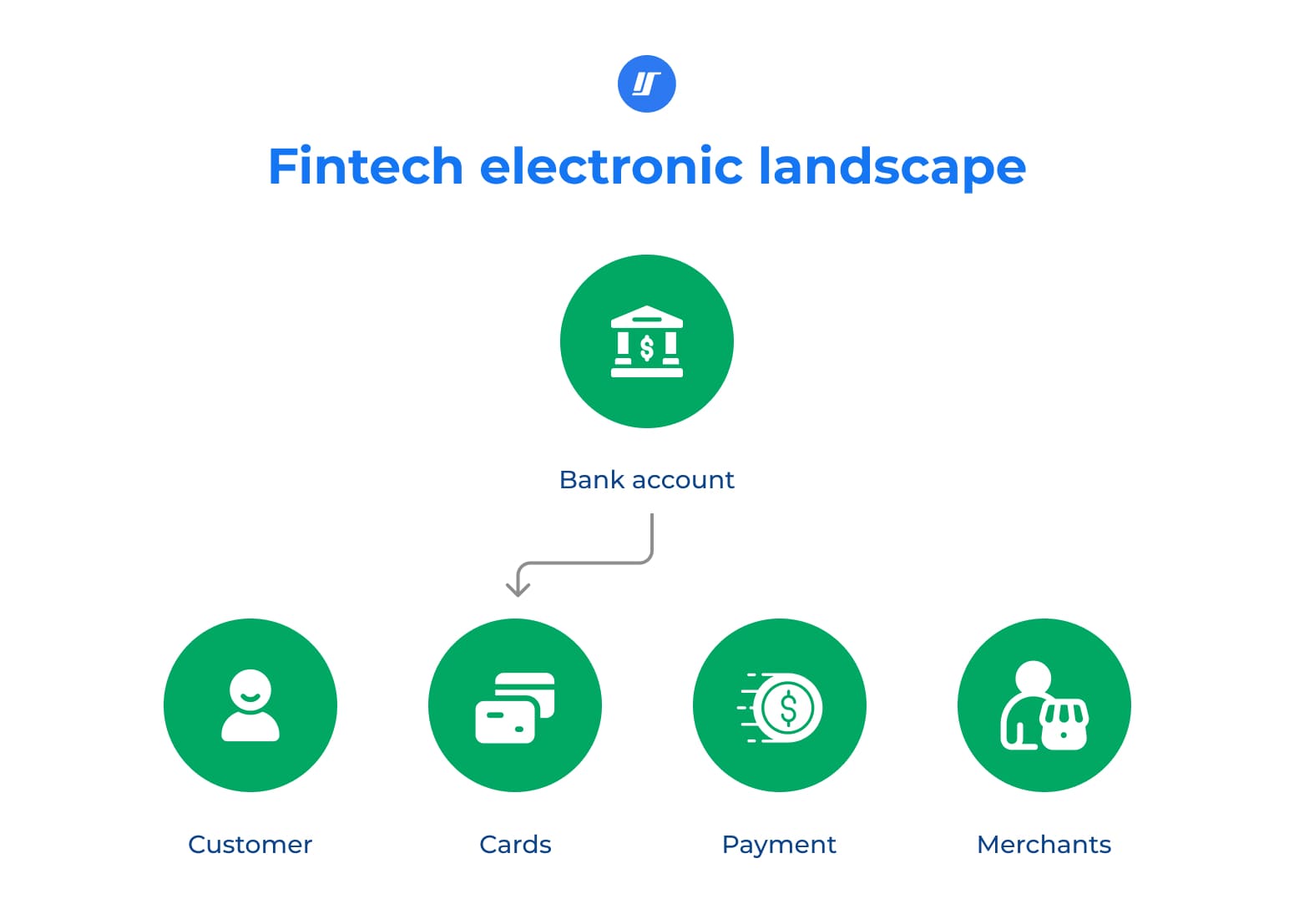

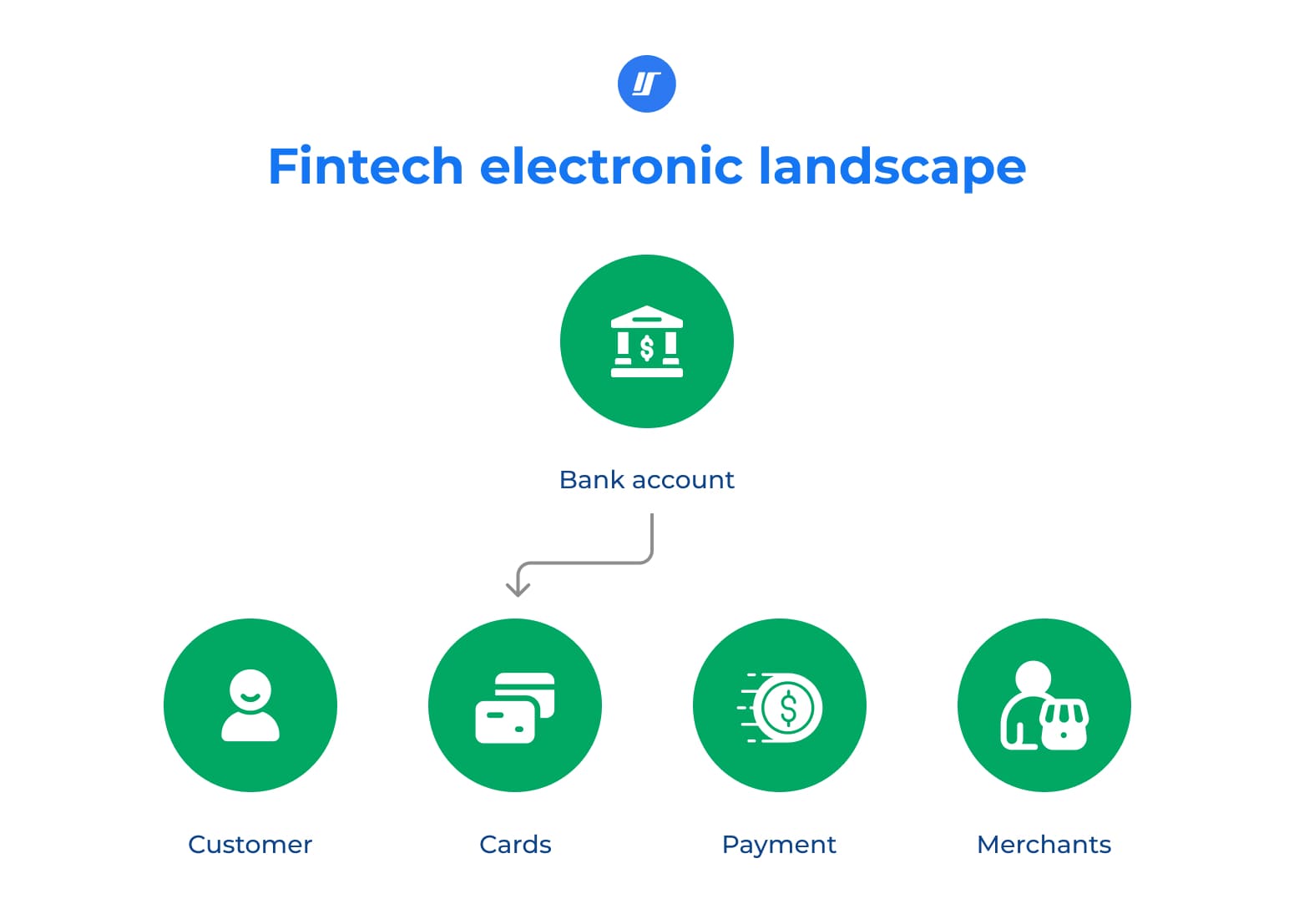

With the advent of FinTech, the world of SME banking is undergoing a tech-savvy makeover.

Imagine a banking universe where every service, every product, is tailor-made, just like a bespoke suit perfectly cut to fit its wearer. FinTech is adding smart, high-tech accessories to that already well-crafted suit. In other words, with SME banking solutions, their financial needs aren't just an afterthought—they're the star of the show.

As a more plastic illustration, picture a quaint local bakery that once spent hours on billing, now effortlessly managing transactions with a sleek digital payment platform. FinTech's integration into SME banking is revolutionizing their game, making financial management not just more convenient but also smarter and more intuitive.

In essence, FinTech isn't just redefining SME banking; it's reinventing it, making it more inclusive, more accessible, and more aligned with the dreams and realities of small and medium-sized enterprises.

Challenges Faced by SMEs in Banking

- Limited access to capital

- High transaction costs

- Cumbersome payment processing

- Complex financial management

- Inadequate personalized services

- Inflexible banking hours and locations

- Credit scoring challenges

- Lack of financial literacy resources

- Data security concerns

- Regulatory compliance

- International transactions

- Delayed invoice settlements

FinTech's innovative approach to these challenges improves the position of an SME in banking. It helps the companies operate more efficiently, scale effectively, and focus on their core business activities.

How FinTech Addresses SME Banking Challenges?

So, this is where FinTech starts as the hero. With SME banking solutions, it revolutionizes how these businesses interact and navigate the finance landscape.

Digital lending platforms, among other perks, are streamlining the loan process. It's like having a financial wizard at your fingertips, turning weeks of paperwork into a few clicks. Take, as an example, a small tech startup that accessed seed funding through a digital platform, catapulting it from a garage to the global stage. Mobile banking and AI-driven financial tools are also part of this FinTech arsenal, empowering SMEs with real-time financial insights and control.

Here is an overview of the most notable FinTech solutions to common challenges.

Access to Capital

Traditional lending can be a tightrope walk for SMEs, with banks often setting a high bar for loan approval. FinTech dances to a different tune, offering platforms like peer-to-peer lending and online crowdfunding, where SMEs can secure funds without the rigmarole of traditional banking.

Transaction Costs

For SMEs, every penny counts, but banking fees can take a big bite out of their budget. FinTech slashes these costs with sleek, automated processes, turning what was once a financial drain into a manageable trickle.

Payment Processing

Juggling payments with old-school systems can feel like navigating a hedge maze for SMEs. FinTech simplifies this labyrinth with swift, user-friendly payment solutions, ensuring SMEs keep their cash flow as fluid as a running stream.

Financial Management

Economic administration can be full of twists and turns. FinTech brings in a GPS in the form of intuitive digital tools that help SMEs easily chart their financial course, from budgeting to forecasting.

Personalized Services

SMEs often crave banking that understands their unique needs rather than semi-usable cookie-cutter solutions. FinTech tailors its suit to fit every SME, offering specialized products and advice that resonate with their individual business models.

Banking Hours and Locations

Traditional banking hours can be a hassle in the contemporary business landscape, feeling like a square peg in the round hole of an SME's schedule. With FinTech's 24/7 online platforms and SME mobile banking, financial management becomes a flexible process suitable to any timeline.

Credit Scoring

Conventional credit scores can unfairly label SMEs, leaving them in the financial cold. FinTech uses a broader lens, considering various data points to paint a fairer picture of an SME in banking, emphasizing their creditworthiness and warming them up to more funding opportunities.

Financial Literacy Resources

Navigating the financial landscape without a map can leave SMEs lost. FinTech provides this map through accessible, easy-to-understand educational resources, guiding SMEs toward better financial health.

Data Security

In a digital world, data leaks are like open floodgates for SMEs. FinTech reinforces the dam with advanced security measures like encryption and blockchain, keeping SMEs' financial data safe and dry.

Regulatory Compliance

Staying on top of regulations can feel like a high-wire act for SMEs. FinTech acts as a safety net, incorporating compliance features that help SMEs adhere to financial laws and standards, all without the circus act.

International Transactions

Global business can tie SMEs in knots with currency and cross-border payment complexities. FinTech untangles these knots, offering streamlined solutions for international transactions, turning a global headache into a walk in the international park.

Invoice Settlements

Late payments can strangle SMEs' cash flow. FinTech offers a lifeline with solutions like invoice financing and digital invoicing, ensuring payments flow as smoothly as a serene river, bolstering the SMEs' financial health.

Through these innovative solutions, FinTech addresses the specific challenges of SME banking, empowering companies to navigate the financial landscape with greater ease, confidence, and success.

Collaboration Between Banks and FinTechs

The evolving tale of banks and FinTech companies relies on partnership and cooperation, where each party brings its strengths to the table. This beneficial fusion thrives on blending the reliability of traditional banking processes with technological innovation.

Among the bountiful case studies, the best examples here might be the FinTech giants themselves. TransferWise, co-founded by Skype alum Taavet Hinrikus, is a prime illustration of FinTech innovation meeting SME needs. Originating from a personal need to avoid high fees in cross-border transactions, once an SME itself has grown into a leading player in the field, offering efficient, low-cost international payment solutions now widely used by other SMEs.

The stories of Lending Club and Revolut further epitomize the fusion of tech-driven solutions and traditional financial services, catering effectively to the global business needs of SMEs.

Opportunities for Growth in SME Banking

The business landscape for small and medium-sized enterprises is changing, closely following FinTech innovations as they unlock new growth opportunities. Digital lending platforms use algorithms to assess creditworthiness, providing quicker and more accessible funding options. This is particularly beneficial for businesses previously overlooked by conventional banks. In addition, personalized banking services involve a variety of integration possibilities and a level of customization that was previously out of reach for many.

Example: A boutique coffee shop with a stellar prospect that may struggle with traditional bank loans due to the nature of its business.

In addition, AI and data analytics are revolutionizing SME banking, transforming guesswork into strategic decision-making. SMEs can leverage these tools for cash flow forecasting and customer spending analysis, enhancing their inventory management and marketing strategies in return. To quote Wealth and Finance, “Thanks to the advent of predictive analytics tools such as machine learning algorithms or modeling software, SMEs can now look at historical data and make projections for what may happen in the years ahead.”

Example: Small construction companies can now streamline their financial operations with customized solutions from a single FinTech platform.

FinTech is also paving the way for SMEs to expand into international markets. Simple, efficient handling of international payments and currency risk management opens global opportunities once hindered by complex banking processes. A study conducted by Chinese experts, based on the data of listed small and medium-sized enterprises from 2011 to 2020, proved that FinTech in banking can significantly ease the financing constraints of SMEs. Their results showed a decrease of 0.0767% for every 1% increase in FinTech.

Example: Small artisanal soap makers or chandleries are often confined to local markets. By utilizing a FinTech platform to seamlessly handle international transactions and manage exchange rates, they gain the opportunity to expand their customer base and reach multiple countries with ease.

The Future of SME Banking

It doesn’t take a crystal ball to detect that SME banking’s future sparkles with FinTech innovation. Technologies like AI, blockchain, and open banking evolve day by day, promising to revolutionize this space further.

SMEs have already begun managing their finances with the help of AI assistants, in addition to using blockchain for secure, transparent transactions. This future is not just a possibility; it's unfolding before our eyes, reshaping the entire banking landscape into a dynamic, tech-savvy ecosystem.

Wrapping Up

In summary, the marriage of FinTech and SME banking is more than beneficial—it's transformative. It's a venture of overcoming challenges and seizing opportunities, where SMEs are no longer bystanders but active players in the banking arena. As FinTech continues to evolve, it's clear that SME banking will never be the same.

In such an inspiring landscape, companies like Intellectsoft emerge as key players with their tailor-made FinTech solutions. They harness their vast global experience to fuel SME growth, providing bespoke financial technology platforms: innovative, practical, and accessible.

Intellectsoft's commitment to delivering top-notch services ensures that its software is seamlessly woven into the fabric of SMEs' business operations, empowering them to navigate the complexness of the global market with confidence and efficiency.

FAQ

How is digital banking for SMEs reshaping the banking landscape?

Digital banking is revolutionizing SME banking, making it more agile, accessible, and user-friendly.

What are the newest innovations in SME banking software?

SME banking services are constantly evolving, with cutting-edge technologies like AI and blockchain leading the charge.

Why should SMEs turn to FinTech for their banking needs?

FinTech offers SMEs a world of advantages - from cost savings to enhanced financial control.